Under modern lending rules, consistent score tracking prevents surprises when applying for financing.

To Use Credit Karma effectively, treat it as a daily trend monitor built on TransUnion and Equifax data, then layer in targeted actions that move the needle.

Scores shown on Credit Karma use the VantageScore model, not FICO, and reflect what those two bureaus currently report. Differences still surface across models and bureaus, so plan for a reasonable range rather than a single “true” number.

What Credit Karma Shows and How It Updates

Across Credit Karma, scores are VantageScore 3.0 values sourced from TransUnion and Equifax, displayed alongside high-level factors such as payment history and credit utilization.

Credit Karma now checks your TransUnion and Equifax reports daily for changes; score movement appears when underlying data updates, which lenders typically send monthly.

Credit Karma vs. Lender Scores: Why Numbers Differ

Because lending decisions frequently rely on FICO versions and may include Experian, expect deltas between Credit Karma and a lender pull.

Model differences (VantageScore vs. FICO), bureau coverage (TransUnion/Equifax only on Credit Karma), and timing explain most gaps. Plan around a variance band rather than fixating on a single point.

Set Up and Secure Your Credit Karma Account

Creating a Credit Karma account takes a few minutes and requires identity verification to access bureau data.

Enable two-factor authentication and keep credentials unique. Credit Karma uses encryption and performs only soft inquiries, which don’t affect scores.

Read Your Dashboard Like an Underwriter

In practical terms, the dashboard surfaces two scores, recent changes, and the top drivers behind them. Payment history issues carry outsized impact, so confirm due dates are current and autopay covers at least the minimums.

The credit utilization ratio, revolving balances divided by limits, follows quickly behind; reductions here can move scores within a single reporting cycle.

New account activity and the depth of history also appear; rapid-fire applications or recently opened cards can suppress numbers temporaril,y even when balances remain modest.

Fast Workflow to Track and Correct

Frequent, lightweight check-ins outperform occasional deep dives. This simple loop keeps your file clean and responsive.

- Review both the TransUnion credit report and Equifax credit report for accuracy, then note the “date updated” lines to gauge reporting cadence.

- Scan factor grades; prioritize missed payments, high utilization, and recent hard inquiries before lower-impact items.

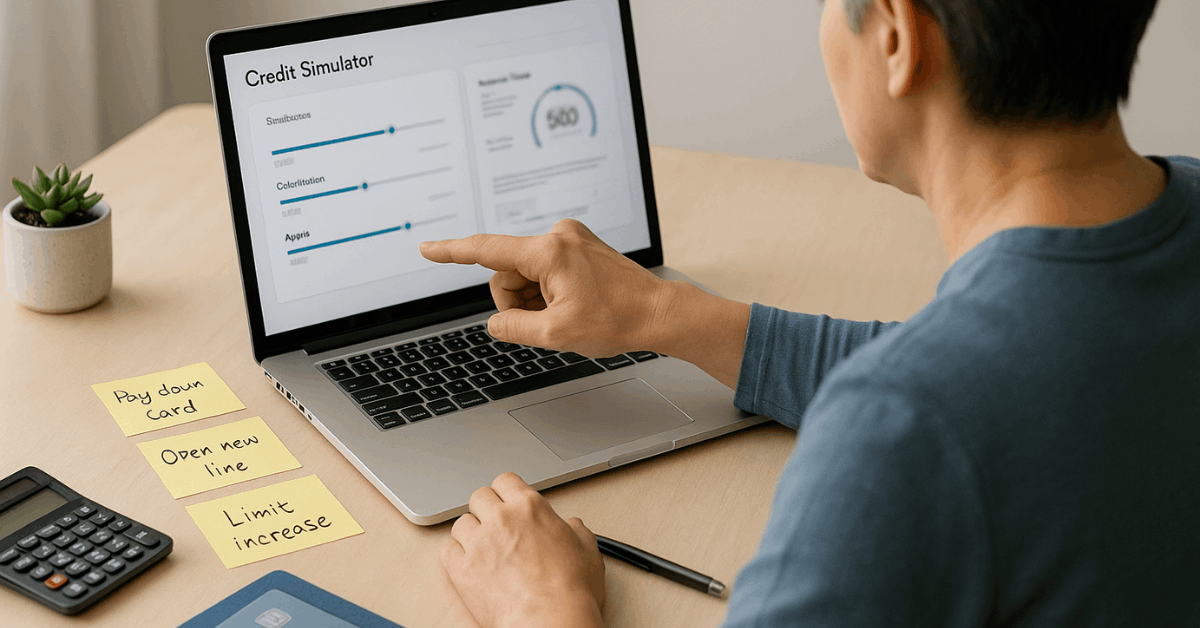

- Use Credit Karma’s credit score simulator to sanity-check actions such as paying down a balance or requesting a limit increase.

- Set identity monitoring alerts so new accounts, inquiries, or data-breach exposures trigger immediate review.

- File disputes directly with the appropriate bureau when inaccuracies appear, attaching statements, payment confirmations, or closure letters as evidence.

Accuracy, Limits, and Smart Expectations

Because Credit Karma displays VantageScore 3.0 from two bureaus, it’s possible to see a number that lands higher or lower than a lender’s FICO pull that includes Experian. That gap commonly stems from model math and reporting timing, not an error.

Treat Credit Karma as a free credit monitoring tool for direction and momentum rather than an exact approval predictor. When preparing for a mortgage, obtain official FICO scores through a card issuer benefit or a direct purchase to align with lender use.

Improve Scores Using Actions That Actually Register

Credit scores respond to behaviors lenders actually report, not quick fixes or myths. Focus on habits that show up in monthly data and persist across multiple billing cycles.

Small improvements compound as they repeat, creating steady upward momentum without gimmicks.

- Pay every bill on time; payment history remains the single largest driver across scoring models. Even one 30-day late can depress scores for years; automatic payments and due-date alignment reduce slipups.

- Lower revolving balances to push utilization below 30%, with sub-10% delivering stronger lift once sustainable. Most issuers report statement balances, so a mid-cycle payment can cut what’s reported before the closing date.

- Keep well-aged cards open to preserve average age unless fees outweigh benefit. When annual fees bite, request a product change to a no-fee option to preserve limit and history.

- Space new applications; multiple hard inquiries in tight clusters can suppress scores temporarily. Rate-shopping windows vary by model and product, so keep comparisons tight in time.

- Diversify accounts only when needed; installment plus revolving forms a healthy mix without unnecessary debt. Opening accounts purely for mix can trigger new-account score hits and unnecessary interest expenses.

Identity and Money Features Worth Knowing

Credit Karma includes breach and new-activity monitoring tied to your credit files, helping catch fraud early.

For banking-adjacent tools, Credit Karma Money Spend and Save accounts are offered through bank partners with FDIC insurance via a deposit network up to stated limits; offerings and rates change, so review current terms inside the app before opening.

Tax filing formerly branded “Credit Karma Tax” moved to Cash App Taxes after a 2020 divestiture tied to the Intuit acquisition, so current tax prep routes may point to TurboTax instead of an in-house product.

Simple Credit Karma Routine for Homebuyers

During mortgage prep, move from casual monitoring to a disciplined cadence. Track balances weekly and project statement-closing dates to ensure low utilization snapshots before each report cut.

Freeze unneeded applications 90 days before pre-approval to minimize fresh inquiries. Compare Credit Karma trends with paid FICO pulls on the same week to understand your personal model gap.

Document disputed corrections; underwriters may ask for proof even after bureau updates. Re-run numbers after large paydowns post to confirm debt-to-income and pricing tiers look favorable.

Conclusion

For day-to-day visibility, Use Credit Karma as a reliable early-warning and coaching system. Daily report checks from TransUnion and Equifax, transparent factor grading, and quick alerts make it easy to spot issues and measure progress.

Model and bureau differences mean the number won’t always match a lender’s pull, yet the direction and drivers will align when habits improve.

Pair that momentum with official FICO checks before major financing, and your file will present stronger when it matters most.